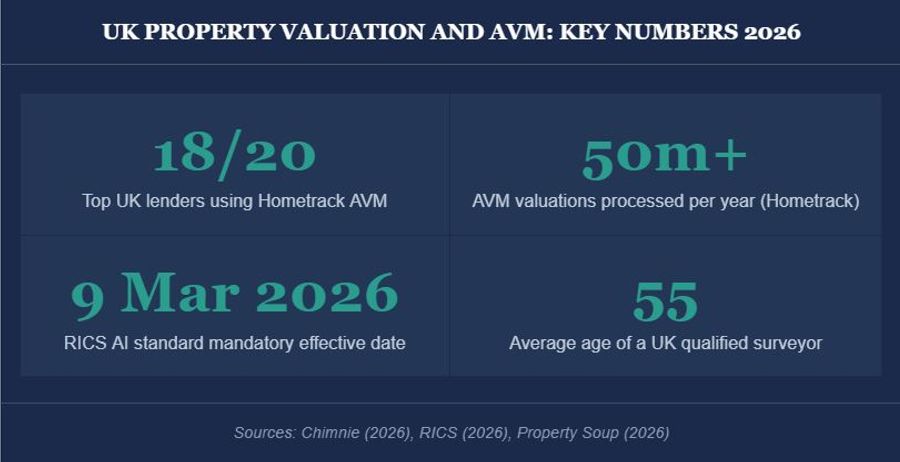

On 9 March 2026, every RICS member and regulated firm became subject to the RICS Global Standard: Responsible Use of Artificial Intelligence in Surveying Practice. It was the first time RICS had made AI governance mandatory across all disciplines. For property valuation professionals, the timing was deliberate. AVMs already sit inside 18 of the UK's top 20 mortgage lenders, processing more than 50 million valuations a year. The standard arrived not as a distant warning but as a catch-up to market reality.

This is not a repeat of the debate about whether machines can value property. That argument is largely settled for standard residential stock. The live questions now are about regulation, professional indemnity insurance, career positioning, and what consumers actually get when they punch their postcode into Zoopla or Rightmove to check their home's value for free. Those questions matter to anyone working in or entering the UK valuation market in 2026.

What the Red Book now says about AI

The current edition of the RICS Valuation Global Standards, known as the Red Book, became effective on 31 January 2025. It made several things explicit. No AVM output, without the application of professional judgement by a registered valuer, constitutes an IVS-compliant property valuation. The wording is stark: 'No model without the valuer applying professional judgement, for example, an automated valuation model, can produce an IVS-compliant valuation.' That requirement did not change in the 2025 update. It was tightened.

The Red Book also introduced a new mandatory requirement to record ESG factors as part of any property valuation. That may sound tangential, but it compounds the AVM problem. Most consumer-facing AVM tools, and many lender AVM platforms, carry no ESG data layer at all. A registered valuer signing off on an AVM-assisted property valuation now needs to satisfy themselves that ESG considerations have been addressed. That is professional judgement work, not a box-ticking exercise.

Alongside the Red Book sits the RICS AI standard, now in force. It requires firms to maintain risk registers for AI tools, responsible use policies, and procurement due diligence for any AI system used in professional practice. For a valuation firm deploying an AVM in its workflow, this means documenting how the model works, where data comes from, what confidence thresholds trigger a physical inspection, and who is accountable when the output is wrong. That is a significant governance overhead that many smaller practices have not yet taken on.

The consumer market: what online property valuation tools actually deliver

The consumer-facing online property valuation market has matured considerably. Rightmove's Instant Online Valuation uses machine learning models trained on HM Land Registry sold prices, Rightmove listing data, and comparable property information, refreshing estimates every 30 days. Zoopla offers monthly house price estimates that track equity and flag remortgage windows. Nationwide's house price calculator uses its own index data and explicitly tells users the figure is a guide that 'won't be used in any Nationwide mortgage application'. Halifax provides valuation guidance through its help-and-advice section, but stops short of a live instant estimate tool.

At the lender infrastructure level, Hometrack dominates. Its AVM carries accreditation from Moody's, S&P, and Fitch, has been embedded in regulated UK mortgage lending since 2002, and has been used in more than 50 RMBS issuances. In early 2026, Selina Finance became one of the first lenders to launch no-valuation mortgage products built on Hometrack's infrastructure, an indicator of how far lender confidence in AVM outputs has travelled. PriceHubble, which competes for the same enterprise market, passed an ISAE 3000 external audit for EBA compliance in 2025 and counts the Bank of England among its UK clients.

The distinction between a consumer online property valuation estimate and a regulated lender AVM output matters enormously. The Rightmove estimate on your screen is directional. The Hometrack output feeding a lender's mortgage decisioning platform carries model validation, rating-agency sign-off, and a confidence score that determines whether a physical inspection is needed. Consumers who confuse the two are forming house valuation expectations that may not survive underwriting.

PI insurance: the questions your insurer is now asking

Professional indemnity insurance for property professionals is currently in a soft market cycle. According to Marsh's July 2025 PII market update, premiums have been falling, coverage limits are growing, and insurers have 'big growth budgets to achieve on their risk books'. That is the good news for firms renewing now.

The catch is AI. Marsh's same update flags that insurers are paying closer attention to technology processes within firms, especially concerning the use of AI and digital tools, and that governance and supervision questions 'will become part of an underwriting assessment'. One or two PI insurers have already started applying conditions and exclusions around AI use. The Marsh team is monitoring this.

The specific questions now being directed at property and construction professionals, according to Browne Jacobson's February 2026 analysis, include: 'How do you validate AI-generated property valuations against comparable market data and professional judgement?' and 'How do you ensure AI valuations account for local market conditions, upcoming infrastructure developments, and neighbourhood factors?' These are not soft questions. If a firm cannot answer them with documented governance, the insurer has grounds to apply an exclusion or adjust the premium. A valuation practice that has integrated an AVM into its workflow without a written validation protocol is exposed.

The professional valuer in 2026 must document how they govern, validate, and override AI tools. That is the PI insurance and Red Book requirement working together.

"What we are looking at before us now is potentially more disruptive to surveying practice than the abolition of fee scales many decades ago. We will need to adjust business models to suit and increasingly articulate the value we add to our clients." Paul Beeston FRICS, Partner and Head of Industry and Service Insight, Rider Levett Bucknall

What this means for a property valuation career path in 2026

The workforce picture is uncomfortable. According to RICS data cited in Property Soup's March 2026 analysis, the average qualified surveyor in the UK is in their mid-fifties. Two-thirds of respondents in recent RICS research cited the ageing workforce and high retirement rates as the main concern. New entrants are not arriving fast enough, and roughly half of younger RICS members say lower starting salaries compared to other STEM fields put them off.

The work itself is polarising. Lenders are using AVMs for lower-risk, straightforward valuations, and that trend will accelerate. The house valuation for a standard semi-detached in a well-transacted suburb no longer needs a registered valuer to do the data-gathering. What it does need is a valuer who can set the confidence threshold, interpret the exceptions, and sign the report. The complex instructions, development appraisals, gross development values, unusual or heritage properties, and cases where the AVM confidence score is too low, are the instructions growing in relative importance. A career in property valuation in 2026 is not under threat. A career spent doing only the work an AVM can replicate is.

There is also the qualification angle. RICS's AI standard explicitly states that AI assists professional practice; it does not replace it. Surveyors remain accountable for every piece of professional advice, regardless of the tools used. That is both a protection for the profession and a requirement. The APC route to MRICS, with its minimum 24 months of structured training and 96 hours of CPD, still exists precisely to produce professionals capable of the judgment calls that no AVM can make. Understanding how to get a property valuation right in the full Red Book sense, including knowing when to override a model output, is the core skill the market will pay for.

RICS is currently preparing dedicated AI guidance for real estate valuation specifically. The global practice guidance 'Artificial Intelligence in Real Estate Valuation' (1st Edition) was issued for public consultation in Q2 2026 and is expected to be published later this year. It will address how AI interacts with professional judgement, how to source and verify AI-generated information, and what governance looks like at the valuation firm level. Responding to the consultation is a genuine opportunity for practitioners to shape standards that will govern their work for years.

The University of Manchester's research showing AVMs reaching 96% accuracy on standard residential stock was covered in issue 53. The headline figure has done its job in shifting the debate. The question now is not whether AVMs can match a valuer on a data-rich semi-detached. It is whether the professional, regulatory, and insurance frameworks around property valuation are keeping pace with what lenders and consumers are actually using. On the evidence of 2025 and early 2026, the frameworks are catching up fast. Anyone who wants to know how to get a property valuation that is both legally compliant and insurer-defensible needs to understand these frameworks. They now apply to every instruction a RICS-regulated firm takes on.

Three things to do now

One. If your firm uses any AVM tool, desktop valuation service, or AI-assisted property valuation workflow, document it. Write down what the tool is, where the data comes from, what the confidence thresholds are, and who signs off on exceptions. That is not bureaucracy. It is your answer when the PI insurer asks.

Two. Read the RICS AI standard. The full document is publicly available and the supporting case studies for valuation are specifically designed to show what compliance looks like in a real practice. If you are a firm leader, the standard's requirements for risk registers and responsible use policies are mandatory, not optional.

Three. Respond to the RICS consultation on AI in real estate valuation when it opens. The guidance being drafted will set the detailed expectations for how valuers use AI tools in practice. For any client asking how to get a property valuation that complies with the new rules, practitioners who have engaged with the consultation will be better placed to give a straight answer. Those who wait for publication and then react are always catching up.

The online property valuation tools that consumers use for a house valuation estimate and the regulated AVM infrastructure inside mortgage lending are converging. The Red Book, the RICS AI standard, and PI insurers are all drawing the same line: the registered valuer's professional judgement is what makes an AVM output into an actual property valuation. That line is the profession's value.

The Responsible with AI programme helps architects, designers, and other built environment professionals develop practical frameworks for integrating AI tools responsibly.